Financial Responsibility In 5 Easy Steps

Guilty of some pandemic impulse purchases? You’re not alone. Since the beginning of the pandemic, e-commerce sales in categories like home gym equipment and subscription services have skyrocketed. Financial responsibility and financial planning have always been important, but for many people, the last few months dealing with COVID-19 has really emphasized this.

But what does that mean? Financial responsibility can seem daunting, but it doesn't have to be — it’s as simple as just living within your means.

But don’t worry! That pair of jeans (or four) you still have sitting in your cart doesn't mean you can’t start working towards more financially sound choices moving forward. In fact, there are some simple steps you can implement today to be more financially responsible.

In this article, we’ll break down why financial responsibility is so important and the top five tips to get you on your way.

Why is financial responsibility so important?

Simply put, to be financially responsible, you just have to spend less than you make to ensure you live within your means. It’s vital to be financially responsible because the choices you make today will impact your future and the future of those you love.

But this doesn’t mean you can’t do the amazing things you want to, like travel or buy a house. If anything, being financially responsible makes all of this more attainable. If you plan right and act carefully, you can still live your life to the fullest before you retire — without the looming credit card bills and financial uncertainty.

5 top tips for financial responsibility

Now that you’ve no doubt been inspired to get smarter with spending, we’re here to arm you with the top tips you need to succeed.

The best part? These tips are easy to implement, and you can start today! From getting a Will prepared, investing in insurance, planning your budget (and more), follow these tips, and you’ll be well on your way to financial success.

Have a budget (and stick to it)

It’s shocking how quickly your morning coffee or an impulse Amazon order can add up, especially if you aren’t paying attention. If you build a budget, you can enjoy these small joys guilt-free and without a heart attack at the end of the month when you’re reviewing your Visa!

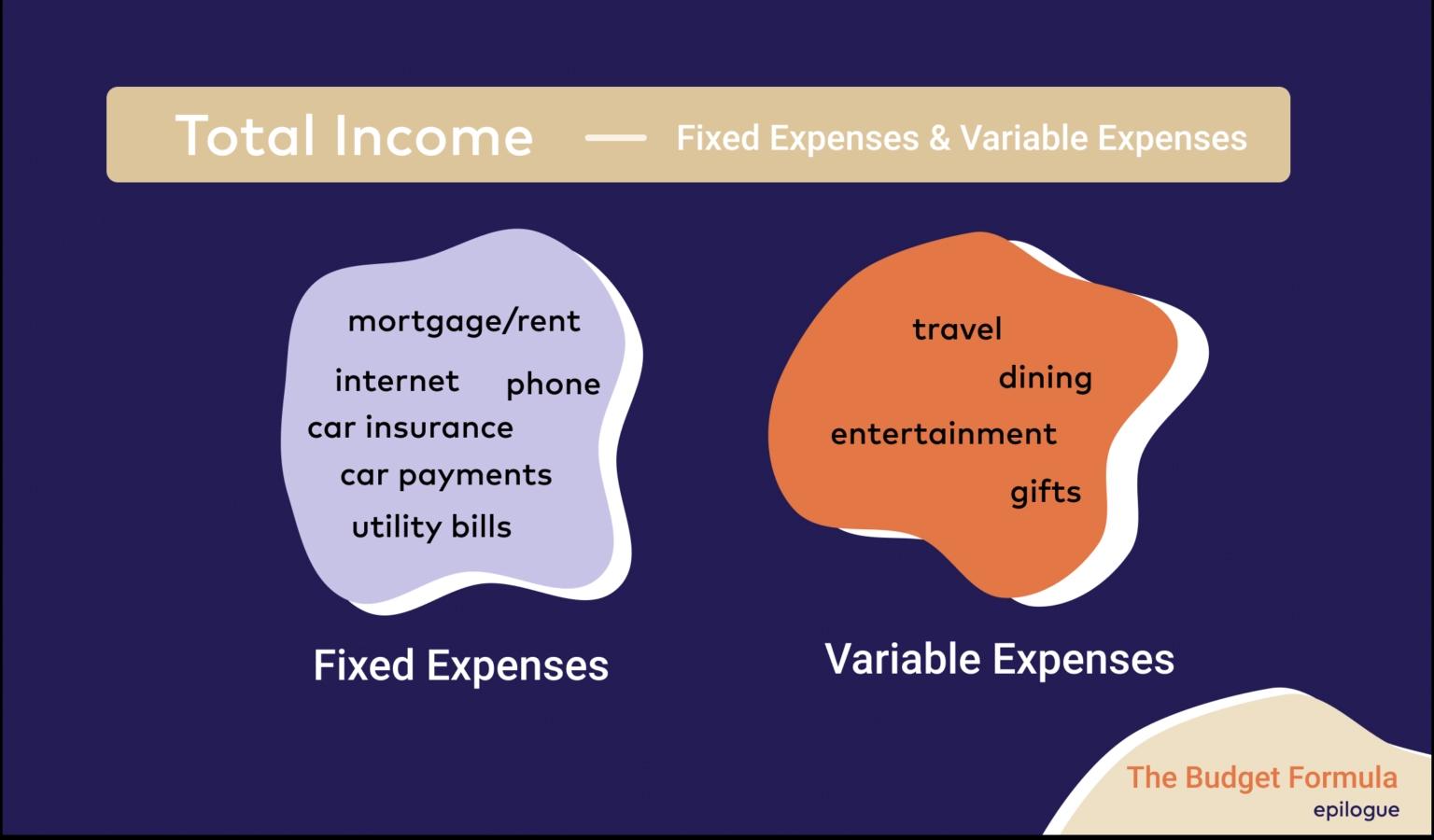

Building your budget isn’t a complicated math equation, either — you can create a simple one within 10 minutes! To make a budget, start with your monthly income. This can be your income alone or added together with a partner’s income if you are sharing expenses.

From there, take a look at your fixed expenses. These expenses are mandatory each month, and – for the most part – stay the same, like rent, car payments, and your phone bill.

After that, you have variable expenses. You’ll want to divide up what’s left after you deduct your fixed expenses from your income among different variable expenses. These are expenses that are optional compared to the ones above and can vary month to month. These expenses could be dining out, entertainment budget, or clothes budget. Your spend within these can change month to month; one month, you could max out your budget on dining out; the next, you may only dine out once. Or, if you’re living through, say, a global pandemic, you might be spending your budget on delivery services like UberEats or DoorDash.

Once you have this set, spend confidently within your budget!

Pay off credit cards on time

Credit cards are an excellent tool for financial responsibility, but they can become a considerable burden if used incorrectly. The interest rates for credit cards sit at 19%, on average, which means for every dollar you don’t pay off, they add another $0.19 to your bill.

That may seem small, but it can add up quickly. Think about it: based on those averages, if you spend $100 on your credit card and don’t pay it off, you’re now looking at $119. If you don’t pay that off, the $119 at 19% interest becomes $141.61. Imagine how fast your credit card bill can start to grow!

If you want to use a credit card, make sure you aren’t putting anything on it that you can’t pay off in the short term.

Have an active savings plan

If 2020 has taught you anything, it’s that emergency savings should be high on your list of financial priorities. With so much unpredictability with health, education, and jobs, having a nest egg is a hugely important part of financial responsibility.

When you do this, you can save for big purchases (like a house or a car) while preparing for a rainy day. When those harder times hit, you don’t have to worry about going into debt to take care of yourself (see how that ties back to paying back a credit card on time?).

Savings can be more passive as well and something that you don’t have to overthink. Most banks will let you set up an automatic withdrawal, where a certain percentage of your paycheque is automatically taken out and moved to a savings account.

Talk to a financial advisor

No doubt, money is complicated. Trying to understand different accounts, RRSPs, RESPs, credit cards — the list may feel like it never ends. And because it’s a complicated concept, it’s no wonder that people can build whole careers around giving financial advice.

Talking to a financial advisor is a great way to gauge the best ways you can save based on your lifestyle, income, and other factors. That’s what they specialize in, and it’s always worth getting an expert’s opinion!

The best part? You don’t have to worry about putting this into your budget because a majority of financial advisors will have at least one conversation with you free of charge.

Protect your loved ones’ financial future

Your financial responsibility directly impacts your loved ones as much today as after you have passed. So you could say you're spending and financial preparedness today has a direct impact on their tomorrow. If you leave behind a lot of debt, it can be a huge financial strain on your loved ones.

The two main ways to make sure you’re managing your money in a way that protects those you love is to get a life insurance plan and keeping an up-to-date Will.

Let’s break both of these down to show you why these are such important parts of financial planning.

Invest in life insurance

Being financially responsible means caring for your loved ones — from parents and partners, to children to anybody else who depends on you financially. The way to do this is by getting a life insurance plan.

Depending on your individual needs, you can get a customized plan just for you. If something happens to you or your partner that leaves you with more expenses than you can afford, your whole standard of living is impacted.

By building a small monthly fee into your budget (and if you’re in good health, you can get life insurance for a great monthly price), you’ll have peace of mind knowing your savvy financial planning goes beyond just taking care of yourself.

Have a Will prepared (and keep it updated)

Another essential part of preparing your loved ones for financial success is to make a Will. Simply put, a Will is a legal document that outlines your wishes about the distribution of anything you own. And while this may not seem like a necessary part of financial planning, there are arguably a lot of benefits of writing a Will that helps to protect your loved ones’ financially. A Will lets people know how you want your money and things distributed and let's you decide who's going to be in charge of carrying out your wishes.

If you die without a Will, all of your stuff gets divided according to the default rules of the province where you live, regardless of what you would have actually wanted to happen.

If you’re a parent of minor children, dying without a Will also means you won’t get to choose who would take care of them if you're not alive or when your children will receive their inheritances. The age of majority in most provinces is 18, which is pretty young for anyone to handle a large sum of new funds. If you make a Will, you can set your kids up for financial success by having their inheritances held by a trusted person until they reach the age of your choice.

These are two small (but crucial!) parts of financial planning that help you care for those you care about the most.

Financial responsibility isn’t a one-and-done thing — it’s something you have to actively work at every day. But with a little preparation and acting on these tips, you’ll be savvier with your spending in no time!

This is a guest post from our partners at PolicyMe, an online platform that helps you compare life insurance policies and purchase one that's best for you.